If you’re buying a property to let out, you’ll want to know exactly how much your monthly mortgage payments are going to cost, and how much you’re likely to be able to borrow.

Our buy-to-let mortgage calculators can crunch all the numbers on your behalf, working out how much your monthly payments will be based on the amount you want to borrow, the rate and the mortgage term you’ve chosen, as well as how much you can borrow based on the monthly rental income you

expect to receive.

Remember that the exact amount you could borrow will depend on several other factors too, such as your outgoings and the amount of deposit you have,so speak to one of our expert advisers to see exactly which deals you’ll be eligible for

.

How much your buy-to-let mortgage will cost you will depend on several

factors. The main ones are:

● Size of your deposit: The bigger deposit you can put down, the smaller the mortgage you'll need to borrow. Lenders will usually ask for 25% of the property’s value, although it can be higher

● Interest rate: You’ll only pay back the interest each month, not the full capital amount

● Loan term: You’ll pay back the full cost of the mortgage at the end of the loan term

With a buy-to-let mortgage, you’ll only usually pay the interest each month, not the full capital amount. But while this might mean your monthly repayments are cheaper than a standard residential mortgage, you’ll need to consider how you’ll repay the full cost of your mortgage debt at the end of the loan term.

You can work out what your repayments will cost you each month. This will be based on how much you’re borrowing, the interest rate and fees of your mortgage deal, and how long you’ll have to pay it off (the term).

What are the benefits of buy-to-let?

Many investors, including those from overseas, look for buy-to-let properties

in the UK. Here are some of the reasons why

Rental income

Generates a steady stream of revenue from tenants, providing a source of

passive income – although the property needs to be properly managed

Capital appreciation

Property values have increased over time in the UK. While there is no

guarantee this will continue, there could be potential for long-term capital

gains

Portfolio diversification

Owning a buy-to-let property can add diversity to your investment portfolio,

spreading risk across different asset classes

Keeps pace with inflation

Property values and rental income can potentially keep pace with inflation,

protecting your investment against eroding purchasing power

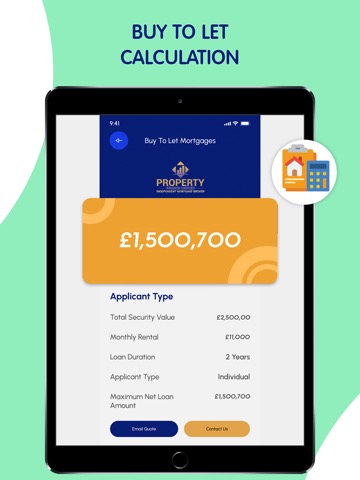

Use our Buy to Let calculator today to see a rough indication on possible solutions, you can then send us a FREE enquiry to be matched to a panel of lenders specialising in this field.

Promotional OFFER - on our 1st - 1000 Enquiries since launching our mobile app we will be waiving all initial fee of $500 to 0!

Simply Quote Buy-To-Let Finance Calculator - Promo’ on your enquiry